We anticipate monitor and comment on market-moving global economic and geopolitical issues. No dark side brooding, no wanting the world to end, no political rants. Traders, investors, policymakers, or market observers can’t afford to ignore us. In one word, perspicacity.

An educated citizenry is a vital requisite for our survival as a free people. – Thomas Jefferson

Wednesday will mark the 83rd anniversary of the start of Joe DiMaggio’s 56-game hitting streak—a record that remains unchallenged in baseball. Similarly, the stock market has exhibited its own streakiness recently, with the Dow Jones Industrial Average closing in the green last Friday, extending its winning streak to eight consecutive days.

Streaky Markets

We find it noteworthy that it has been only 13 trading days since we posted our analysis, “S&P 500 – Will the 20-week MA Hold After Six Straight Down Days?” In that piece, we provided an in-depth look at losing streaks, noting the rarity of such occurrences. For instance, since 1950, the S&P 500 has only registered a 6-day losing streak in 1 percent of the trading days, and just 0.42 percent since 2000.

Dow Streaks

The table below illustrates that the Dow Jones Industrial Average has experienced an 8-day winning streak on only 183 occasions since 1900, which represents just 0.55 percent of the over 33,000 trading days. Our data indicate that the Dow typically closes lower the following day, demonstrating a regression to the mean.

House/Market Odds

It’s interesting to note that the Dow and S&P 500 generate a positive daily return 52.46 percent and 53.03 percent of the time, respectively. These odds are roughly equivalent to the casino’s advantage when betting it all on black or red in roulette. Betting against the market—or the house—never pays in the long run.

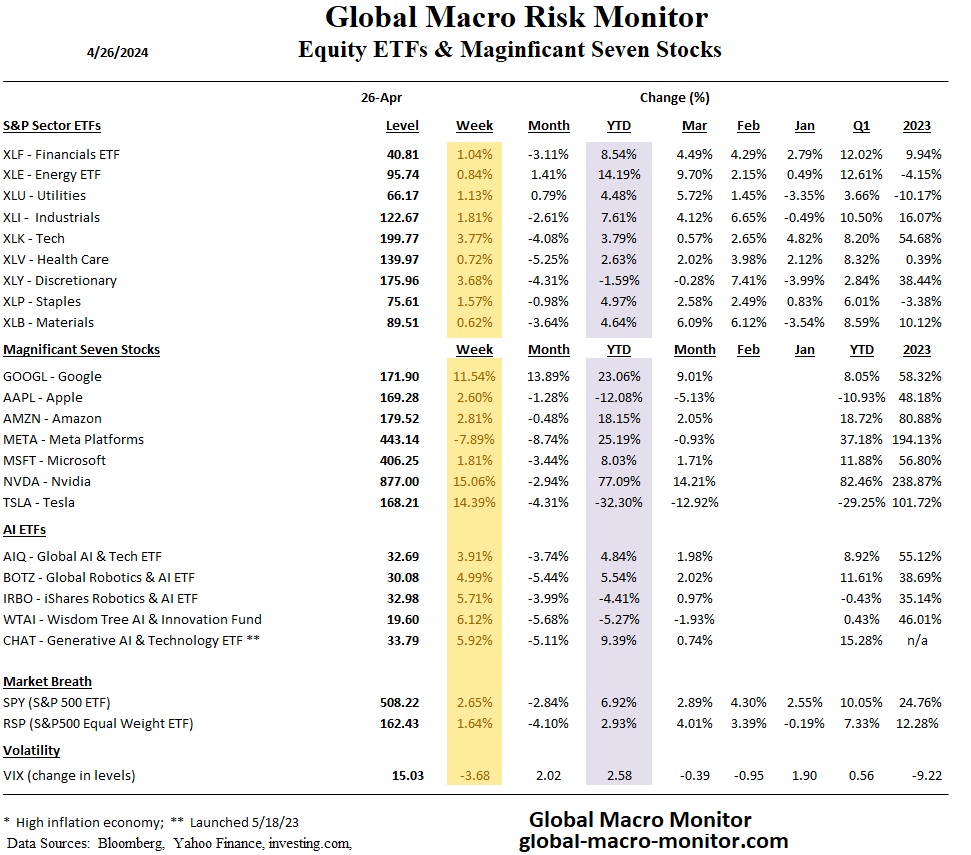

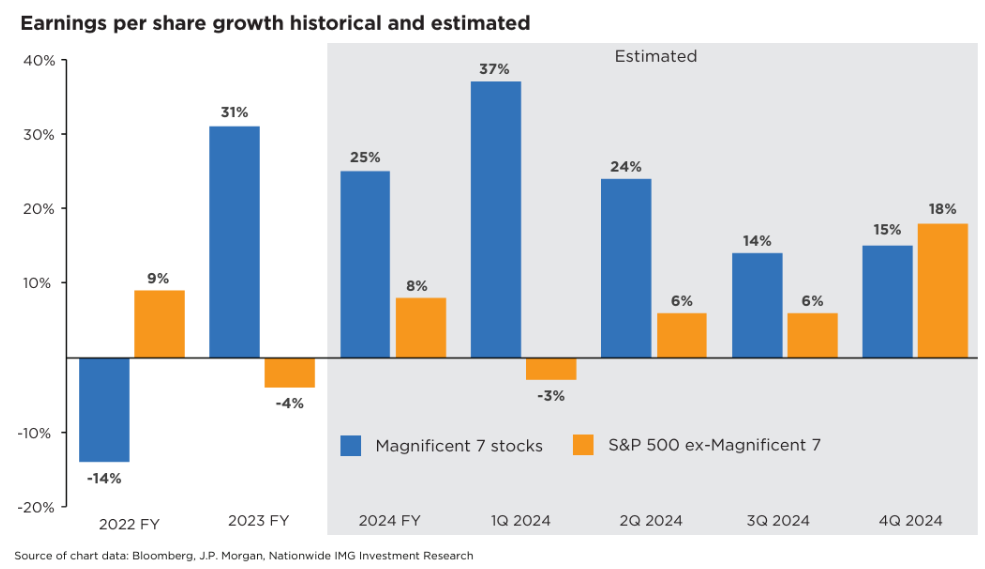

While the cohort of seven megacaps has done well in the last two years because of their superior earnings-per-share growth relative to the broader market, this advantage could decrease in 2024 and even more significantly in 2025, Hackett noted.

“The Magnificent Seven are not nearly as powerful as they once were, and this broadening of the market is creating pockets of opportunity for the rest of the S&P 500,” he noted. “We see this as a positive development for investors looking to diversify away from the recent market leaders,” he added. – Bloomberg

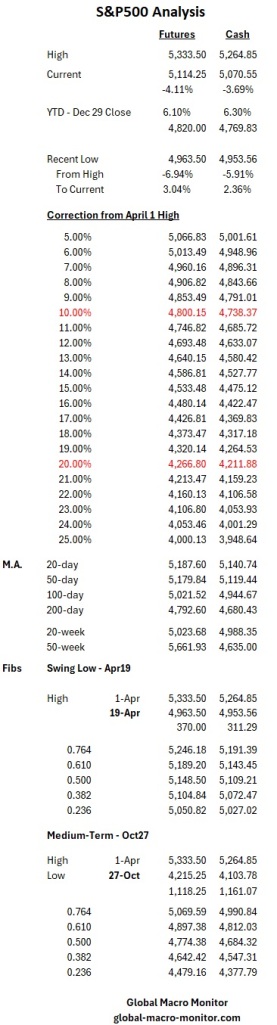

The cash S&P 500 has regained 37.6 percent of its 311.28-point decline from the high on April 1st. The index closed today slightly below a critical 0.382 Fibonacci retracement level. If the futures maintain their bump in after-hours, a reaction to Tesla’s earnings announcement, this level will be taken tomorrow morning.

Nobody knows the future; the best approach for us is to use the analysis of historical data and past levels as a guide to navigate an uncertain and foggy future.

Given the current market narrative of higher for longer, we maintain our view that the S&P 500 is destined for its 200-day moving average of around 4,680.43 before this downdraft concludes. We will reassess if the cash index takes out the .50 Fib level at 5119.44.

We anticipate monitor and comment on market-moving global economic and geopolitical issues. No dark side brooding, no wanting the world to end, no political rants. Traders, investors, policymakers, or market observers can’t afford to ignore us. In one word, perspicacity.

We anticipate monitor and comment on market-moving global economic and geopolitical issues. No dark side brooding, no wanting the world to end, no political rants. Traders, investors, policymakers, or market observers can’t afford to ignore us. In one word, perspicacity.